|

|

|

|

BK Opportunities

Fund 4

Quarterly Report | 31st December 2022

|

|

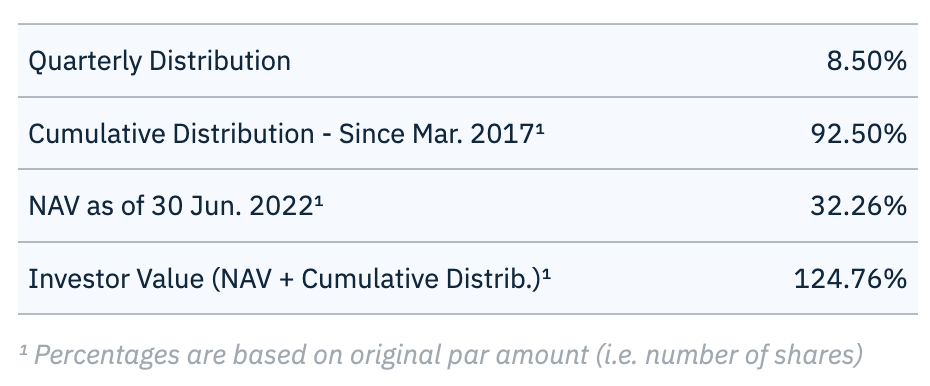

BK Opportunities Fund-4 is making a quarterly distribution to its investors for the 31st December 2022 quarter-end of 8.5% (cash on cash, non-annualized) of its capital contribution (in USD). Payments will be wired on the 3rd of February, 2023.

|

Furthermore, the N.A.V. of BK Opportunities Fund-4 as of the 31st of December 2022, after the distribution, is 32.26% of its capital contribution (in USD).

|

|

BK Opportunities Fund-4 updated performances are:

|

|

December 2022 Monthly Return (non-annualized): -0.7%

|

|

December 2022 Year-to-Date Return (non-annualized): +3.0%

|

|

December 2022 Annual Return since inception(1): +5.6%

|

|

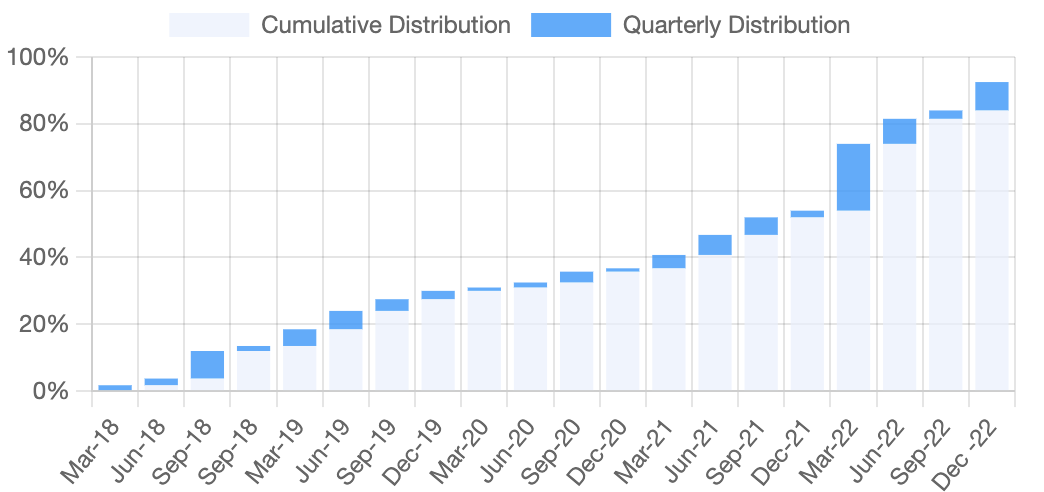

Cumulative Distributions since inception/Mar. 20172: 92.5%

|

Cumulative Return since inception/Mar. 2017 (Distributions + NAV gain)(1): +24.8%

|

|

(1) Based on the weighted average return of all classes since their respective closing date.

|

|

Market Commentary & Portfolio Overview

|

|

|

|

|

The surprisingly abrupt end of the zero COVID policy in China provided the world economy with a boost. The normalisation of the economic conditions in China eased many breaks in international trade. Aside from inflation, the US economy shows signs of resilience.

|

|

|

|

|

|

|

The Economy: Beating Expectation

|

|

Beating expectations, the gross domestic product rose at a 2.9% annualized pace, down from 3.2% in the third quarter. Few reports on labour markets pointed toward a resilient economy. The latest report showed annual inflation was 6.5% in December. Even if inflation is still uncomfortably high, this is the sixth month of the rate falling, pointing toward an improvement. The Fed is expected to hike rates by another 25 basis points next week. Investors' consensus is that the Central Bank is approaching the end of its tightening cycle. Dissident voices are heard, and Fed officials are signalling that rates will stay high until inflation is beaten. The scenario for a “soft landing” of the US economy is becoming much more realistic than ever before. In this scenario, tighter monetary policy cools household spending and lowers inflation – but avoids squeezing the economy so hard that it ignites mass layoffs nationwide. The only cloud in this picture is consumer spending. While consumer spending on services drove the economy to solid growth in the fourth quarter, there is concern that consumers will slow down.

|

|

|

|

|

|

|

Corporate Markets: Uneven Earnings

|

|

Even if GDP is solid, many companies are adapting to the new world order. Big tech started laying off. For example, Google announced a staff reduction of 12,000 people. It is important to remember all those companies kept hiring for many years, and after those layoffs, Google still has more employees than last year. Oil majors also announced losses on the back of low energy prices from the last quarter. It can be interpreted as the adaptation to the end of cheap money and the future global growth perspective. It is consistent with the idea that many underperforming companies did not display their true value in a low-interest rate environment but started to now re-adjust. The timing for the massive short against the companies linked to Indian billionaire Gautam Adani is a symptom of this trend to go back to realistic valuation. Overall, US corporations are well positioned to gain from a more stable and possibly healthier world economy. China re-opening opens to perspective to trade and tourism growth.

|

|

|

|

|

|

|

Corporate Loans: Stabilisation

|

|

The S&P/LSTA default rate has continued to decrease since September to 0.68% by issuer number and only 0.72% by principal amount. We are still very much below industry averages. Corporations have been able to adapt to inflation and to the new world order. Their strong balance sheet and the better economic environment helped their credit situation.

|

|

|

|

|

|

|

CLO Market: Continuum Market

|

|

Total U.S. CLO new issue volume for 2022 was $129.32 billion, far short of the all-time record $187 billion seen in 2021. New issuance volume in 2023 is likely to range from $100 billion to $120 billion as CLO tranche spreads tighten somewhat from their current levels but remain much wider than historical levels. U.S. bank treasury departments, which took a low profile for the last two years, are likely to re-enter the market gradually. The relative value versus other asset types and competing demands for money inside the banks should drive this interest. Current open CLO warehouse lines may support CLO new issuance in the first half of 2023, especially if loan prices rally. CLO resets and refinancings should resume once CLO tranche spreads narrow. 2023 level of reset and refinancing issuance may exceed the average of 2022.

|

|

|

|

BK Opp. Fund 4

|

|

BK Opp. Fund-4 is making a distribution of 8.50% ($85.00 per share) this quarter (payments are being wired on the 3rd of February 2022), bringing the total distribution since inception at 92.50% ($925.00 per share) non-annualized. The cumulative return as of 31st December 2022, which blends distribution and NAV profits, is +24.7%. Based on the weighted average internal rate of return (IRR) of all classes since inception at their respective entry price, BK Opp. Fund-4 annual return is +5.6% (all returns are net). As the fund has been amortizing for 18 months, the main focus is to monetize the remaining positions.

|

|

|

|

|

|

|

|

Quarterly Summary

|

|

|

|

|

|

Fund and Market Performances as of 31st December 2022

|

|

|

|

|

Monthly Performances

|

|

|

|

|

Cumulative and Quarterly Distribution

|

|

|

|

|

|

|

|

Fund’s Summary

|

| Currency |

USD |

| Fund’s Inception |

April 2017 |

| Last Closing |

July 2018 |

| Maturity5 |

July 2023 |

| Distribution |

Quarterly |

| Investment Manager |

Oristan Ireland DAC |

| Administrator |

Apex Funds Services |

| Custodian |

CIBC Bank & Trust |

| Counsel |

Dillon Eustace |

| Auditor |

Deloitte |

| Bloomberg Page |

BKOPP4A KY |

|

|

(5) Excluding the possible 2‐year extension

|

|

|

|

Portfolio Manager

Olivier Gozlan

|

|

|

|

|

|

|

|

|

|

This is not for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to law or regulation. The information contained herein is for information only and does not constitute an offer regarding any product. The document has been prepared by Oristan Ireland DAC and the data have not been audited nor verified. Past performance cannot indicate future performance. There is no assurance that the investment objective will be achieved and investment results may vary.

|

|

|

|

|

|

|

|