|

|

|

|

BK Opportunities

Fund 7

Quarterly Report | 31st December 2022

|

|

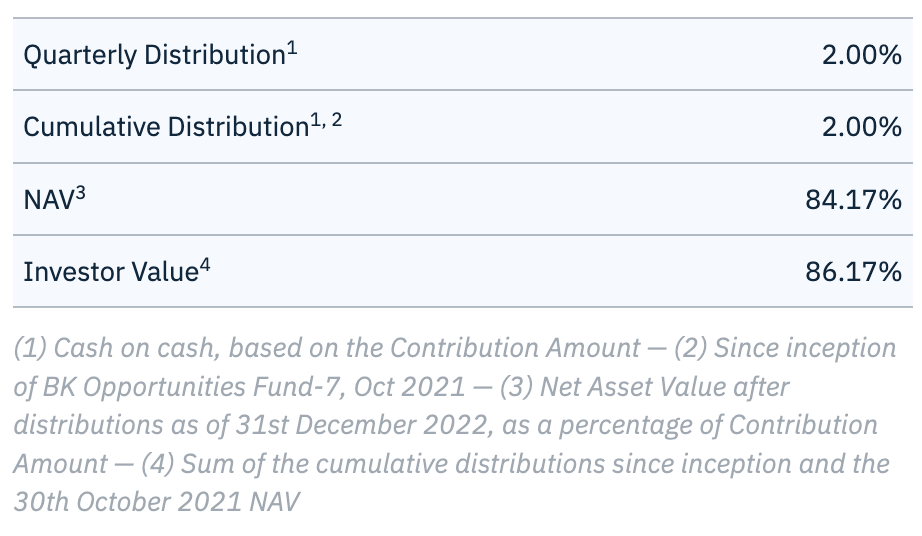

BK Opportunities Fund-7 (Euro) will make its first quarterly distribution to its investors for the 31st December 2022 quarter-end of 2.00% (cash on cash, non-annualized) of its capital contribution. Payments will be wired on the 31st of January, 2023.

|

Furthermore, the N.A.V. of BK Opportunities Fund-7 (Euro) as of the 31st of December 2022 after the distribution is 84.17%.

|

|

BK Opportunities Fund-7 (Euro) updated performances are:

|

|

December 2022 Monthly Return: 1.3%

|

|

December 2022 Year-to-Date: -17.1%

|

|

December 2022 Annual Return since inception1: -8.2%

|

|

Cumulative Distributions since inception/October 2021: +2.0%

|

|

Cumulative Return since inception/October 2021: -13.8%

|

|

|

(1) Based on the weighted average internal rate of return (“IRR”) of all classes from their respective closing date, at their respective entry price

|

|

Market Commentary & Portfolio Overview

|

|

|

|

|

The surprisingly abrupt end of the zero COVID policy in China provided the world economy with a boost. The normalisation of the economic conditions in China eased many breaks in international trade. At the same time, the unexpected low energy cost and mild winter temperatures avoided many of the bleak scenarios.

|

|

|

|

|

|

|

The Economy: The ECB is sticking to their Guns

|

|

The euro area's annual inflation was 9.2 % in December 2022, down from 10.1 % in November; lower energy costs mostly drove this decrease. Even if the direction of inflation is good, it is still seen as the main risk for the euro economy above the Ukraine war, supply chain issues or policy spillovers. Given that inflation is closer to 10% than the ECB mandate of 2%, the first ECB policy meeting of 2023 will almost certainly deliver the half-point hike President Christine Lagarde promised in December. After the January hike, the following increase will probably be more gradual. Council members will be attentive to check whether the rate increase will counter inflation before changing their stands.

|

|

|

|

|

|

Corporate Markets: Confidence Rises

|

|

This quarter has seen the unexpected consumer confidence rise in euroland. Mild winter temperatures, low energy prices and easing supply-chain constraints have provided a supporting hand to the European economy. Optimism is back, and the currency bloc shows some resilience with a low level of (or no) growth this year. This is often called the 0+ or 0- growth expectation for 2023. On the downside, labour strikes can be seen in France, Germany to Italy as an indicator that workers are in crisis. The future is still uncertain as the European economy is linked to the Ukraine war development and energy prices. Overall the growth outlooks are improving.

|

|

|

|

Corporate Loans: Normalization

|

|

Corporate default rates are still well below historical levels, even if the economic story is not rosy. We expect default rates to come toward normalisation and moderate increases. The magnitude will depend on the economic direction of the continent, and the specific story of each corporation, as the end of the cheap money supply, will hit badly managed companies.

|

|

|

|

CLO Market: Low Volume

|

|

New European CLO issuance fell by more than 30% to €26 billion in 2022. Appetite for leveraged finance originations declined to a decade low as corporate borrowers' appetite for debt waned in the higher interest rate environment. CLO volumes could fail to increase in 2023. With CLO liability spreads widening through 2022, collateral managers had no economic incentive to refinance or reset transactions that exited their non-call periods. Refinancing and reset activity shall resume once spread tighten.

|

|

|

|

|

|

|

BK Opp. Fund 7: Performances

|

|

This quarter, BK Opportunities Fund-7 is making its first distribution. This one will be of 2.0% and distribution will now occur quarterly. Payments will be wired on the 31st of January, 2023. Although the asset’s payment has been strong this quarter, we have allocated a portion of the money received for reinvestment, as we believe current prices are an opportunity to boost the fund’s performance. The annual return since inception is -8.2%, well below our expectation but our portfolio is well positioned to resist downside while performing in most anticipated scenarios (even with an increase of defaults). With the current market environment, and despite the robustness of our portfolio, our positions are priced relatively conservatively. As we collect coupons & principal (and distribute or reinvest them) and trade around our positions, the fund’s performance should increase and reach level closer to our target return.

|

|

|

|

|

|

|

Fund and Market Performances as of 31st December 2022

|

|

|

|

|

Monthly Performances

|

|

|

|

Quarterly Distribution

|

|

|

|

|

Vintage

|

|

|

|

|

|

Fund’s Summary

|

| Currency |

EUR |

| Fund’s Inception |

October 2021 |

| Distribution |

Quarterly |

| Investment Manager |

Oristan Ireland DAC |

| Administrator |

Apex Funds Services |

| Custodian |

CIBC Bank & Trust |

| Counsel |

Dillon Eustace |

| Auditor |

Deloitte |

| Bloomberg Page |

BKOPP7A KY |

|

|

Portfolio Manager

Olivier Gozlan

|

|

|

|

|

|

|

|

|

|

This is not for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to law or regulation. The information contained herein is for information only and does not constitute an offer regarding any product. The document has been prepared by Oristan Ireland DAC and the data have not been audited nor verified. Past performance cannot indicate future performance. There is no assurance that the investment objective will be achieved and investment results may vary.

|

|

|

|

|

|

|

|

|