|

|

|

|

BK Opportunities

Fund 5

Quarterly Report | 30th June 2022

|

|

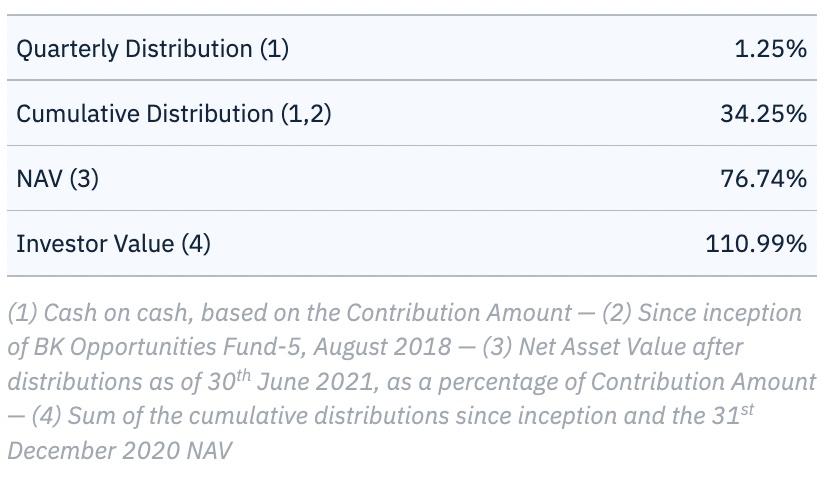

BK Opportunities Fund-5 (Euro) will make its quarterly distribution to its investors for the 30th June 2022 quarter-end of 1.25% (cash on cash, non-annualized) of its capital contribution. Payments will be wired on the 3rd of August 2022.

|

Furthermore, the N.A.V. of BK Opportunities Fund-5 (Euro) as of the 30th June 2021 after distribution is 76.74%.

|

|

BK Opportunities Fund-5 (Euro) updated performances are:

|

|

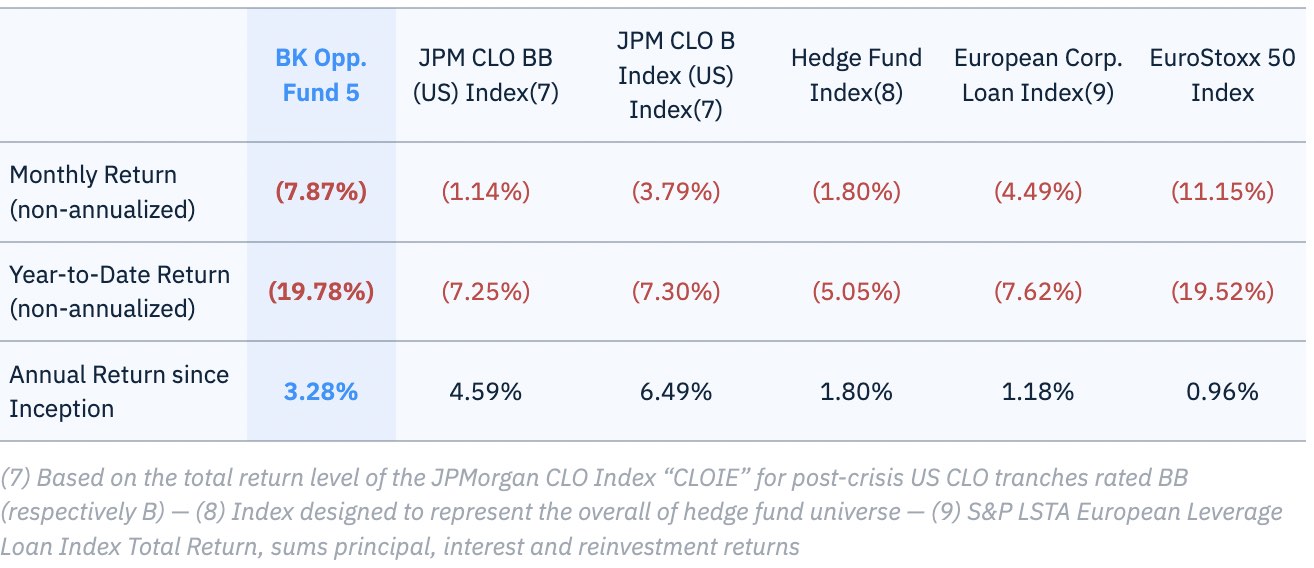

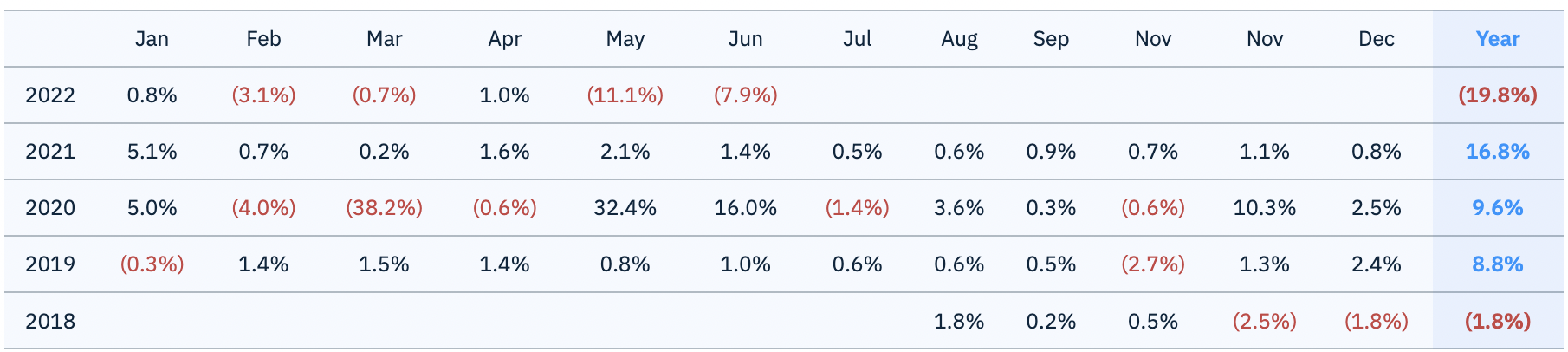

June 2022 Monthly Return (non-annualized): -7.9%

|

|

June 2022 Year-to-Date (non-annualized): -19.8%

|

|

June 2022 Annual Return since inception1: +3.3%

|

|

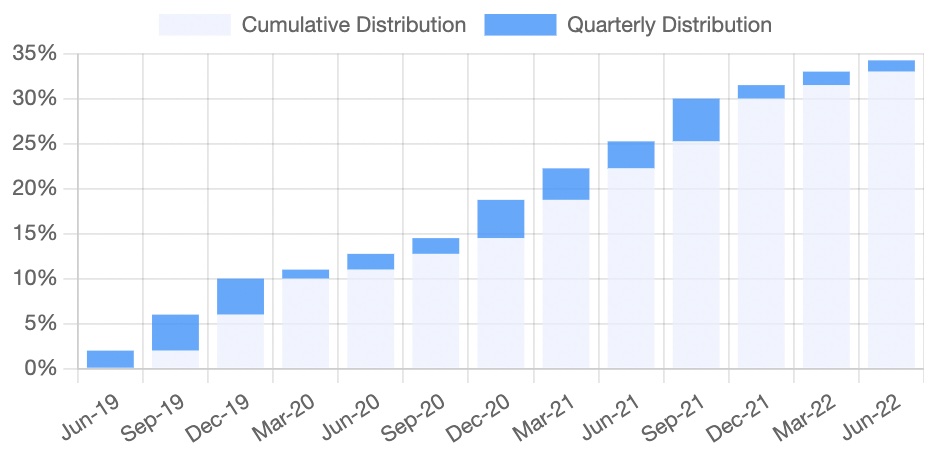

Cumulative Distributions since inception/July 20182: +34.3%

|

|

Cumulative Return since inception/July 20182 (Distributions + NAV gain): +11.0%

|

|

|

(1) Based on the weighted average internal rate of return (“IRR”) of all classes from their respective closing date, at their respective entry price

|

|

(2) Based on the number of shares (or the capital contribution) in the fund i.e. assuming an entry price of €1,000 per share or 100.0%

|

|

Market Commentary & Portfolio Overview

|

|

|

|

|

Many clouds gather around Europe from the continuing war in Ukraine, challenging access to Russian gas, decreasing currency to Italian political turmoil. This is in this uncertain environment that businesses are navigating, but we expect to be able to steer through those unsettled times toward new opportunities.

|

|

|

|

|

|

|

The Economy: Fasten your seat belt!

|

The euro-dollar parity pushes up oil prices that fastens inflation. Russia is decreasing gas delivery, and the perspective of winter with reduced Russian gas supply is getting real. Finally, Mario Draghi resigned, putting the third economy into political turmoil.

|

President Christine Lagarde insists the ECB is "data dependent", but inflation is at a record 8.6% and climbing. Even if the ECB had been very quiet, cautioning that a decision about raising interest rates wasn't taken until a ''surprise'' 50 basis point hick was implemented corresponding to the market expectation. Much speculation is running about the probable September increase. The usual argument is to raise interest rates fast enough to tame inflation but not too fast to kill a recovery. Traders and central bankers are very much split about the magnitude of the appropriate next rate hike. The additional issue with the ECB is the perception that it proves its credibility to its words. A loss in credibility could harm ECB's ability to make believable commitments to investors in future. A short-term recession seems to be the most realistic scenario.

|

|

Another area of disagreement is the future price of oil, further supply disruption due to the Ukraine war could push prices to $135 per barrel, as Goldman Sachs forecasts. At the same time, a depressed economy would bring back prices to $45, as Citi forecasts. In this case, oil prices would directly result from the state of the world economy (and not the opposite).

|

|

|

|

|

|

Corporate Markets: Creative Destruction

|

|

The economy is slowing down on the macro front, and a recession is probable. As a direct result of supply disruption and interest rate increase, the corporate environment is getting less favourable. After a long period of cheap money and good trading conditions, corporates’ margins will now be hurt. So we are expecting an increase of defaults following the current market repricing. It will create some short-end pain but also cleanse the economy of underperforming companies allowing for better performance in the medium range. One of the very few positives of the Covid pandemic has been to force corporations across the board to strengthen their balance sheet to cope with the pandemic. Corporations still enjoy a low-interest rate agreed upon two years ago that should last, on average, another 2 to 3 years. As of today, balance sheets are still healthy and able to cope with worse market conditions.

|

|

|

|

Corporate Loans & CLO: Opportunities

|

|

As a result of the complex environment, corporate debt issuance is 32% lower than last year. Following Credit Suisse European Leveraged Loan Default Rate trailing 12 months rate has stayed constant at 0.2%. An increase of defaults is almost inevitable given the unprecedented low default rate combined with a more challenging business situation. The magnitude of the rise seems to be already priced in, especially for double B and single B markets, providing some opportunities to buy CLO loans at a large discount and selecting the one providing very robust protections from their structural features. Overall the corporate loan situation will worsen, but it should stay manageable and allow us to use our skills to pick up valuable CLO tranches at lower prices, with a very strong resilience level.

|

|

|

|

|

|

|

BK Opp. Fund 5: Performances

Challenged in short term, unchanged for long term

|

|

This quarter, BK Opportunities Fund-5 is making a distribution of 1.25% to its investors. Payments will be wired on the 3rd of August 2022. Although the asset’s payment has been strong this quarter (over 3.3% received), we have voluntarily reduced the fund’s quarterly distribution and increased our allocation for reinvestment, as we believe current prices are an opportunity to boost the fund’s performance. The total distribution since inception at 34.25% of the Capital Contribution. The cumulative return as of 30th June 2022, which blends distributions and NAV profits, is 11.1% or 3.3% on an annual basis. Recent price movement has negatively impacted the mark-to-market of the fund, but our anticipations for the fund’s overall return are unchanged. We continue to monitor market flows and fundamentals and are constantly considering opportunities.

|

|

|

|

|

|

|

Fund and Market Performances as of 30th June 2022

|

|

|

|

|

Monthly Performances

|

|

|

|

Quarterly Distribution

|

|

|

|

|

Cumulative and Quarterly Distribution

|

|

|

|

|

|

Fund’s Summary

|

| Currency |

EUR |

| Fund’s Inception |

August 2018 |

| Last Closing |

October 2019 |

| Maturity(5) |

October 2024 |

| Distribution |

Quarterly(6) |

| Investment Manager |

Oristan Ireland DAC |

| Administrator |

Apex Funds Services |

| Custodian |

CIBC Bank & Trust |

| Counsel |

Dillon Eustace |

| Auditor |

Deloitte |

| Bloomberg Page |

BKOPP5A KY |

|

|

(5) Excluding the possible 2‐year extension

|

|

(6) First quarterly distribution made on 30th June 2019

|

|

|

Portfolio Manager

Olivier Gozlan

|

|

|

|

|

|

|

|

|

|

This is not for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to law or regulation. The information contained herein is for information only and does not constitute an offer regarding any product. The document has been prepared by Oristan Ireland DAC and the data have not been audited nor verified. Past performance cannot indicate future performance. There is no assurance that the investment objective will be achieved and investment results may vary.

|

|

|

|

|

|

|

|

|